ServiceNow's Partner Math: 1 SI = 11% of Revenue (+$4.7B Cloud Commits)

Hi, it’s Roman Kirsanov from the Partner Insight newsletter, where I deconstruct winning Cloud GTM strategies and the latest trends in cloud marketplaces.

In today’s newsletter:

ServiceNow’s partner focus is wild: one SI drives 11% of revenue; ServiceNow also disclosed $4.7B in cloud obligations. We’ll break down their scaling playbook (>20% growth) and why “indirect” can become the default in some segments.

Co-sell is a math problem: cloud sellers often carry $50–$100M books and don’t have time for everyone. Use this 5-Minute Intro to stop getting ignored.

Microsoft hit $625B in total commercial backlog (+110% YoY) with Azure growing 39%—plus why Satya is betting agents become the new apps.

AI is shifting TAM from 1% of GDP (software) to 20% (labor)—and why partners become the rollout moat in an agentic world.

Want to be featured? Partner Insight newsletter reaches 5,000+ Cloud GTM leaders weekly—I’m opening a small Contributor Circle for operator playbooks + templates (details below).

Before we dive in — if you’re not a subscriber yet, subscribe (free). And if this issue is useful, please forward this newsletter to your alliance lead or cloud/GTM counterpart — it’s how this community shares what works.

ServiceNow playbook: one SI = 11% revenue; $4.7B commits

Rule of scaling in 2026: you don’t scale alone.

ServiceNow: one SI drives 11% of revenue; they have $4.7B in cloud commitments, while hyperscaler adoption is shifting their business mix.

ServiceNow still growing >20% at $15B+ scale — in a market that’s questioning whether non-native AI software can grow at all.

They just reported a better-than-expected Q4, 21% subscription revenue growth, and RPO up 25% (21% in CC). That’s a demand signal, not a narrative.

Here are the partnership lessons hiding in plain sight:

1️⃣ Partners are core to their revenue

ServiceNow discloses that an “increasing portion of revenue flows through partners”.

That’s a shift many companies talk about, but few admit in black-and-white.

2️⃣ Some segments are structurally indirect (& concentrated)

They explain that a substantial majority of U.S. government sales are indirect via distributors, resellers, and service provider partners.

One U.S. federal channel partner / systems integrator represented 11% of total revenue.

This is the part alliance teams often underestimate: in some segments, the partner isn’t just helping close deals - the partner is the buyer-facing GTM default.

3️⃣ Hyperscaler adoption is so strong, it changes business mix

They specifically called out a mix shift from on-prem to hosted that was “partially driven by strong adoption of hyperscaler offerings.”

That reframes hyperscaler GTM as more than distribution: It changes how customers buy and consume your platform.

4️⃣ ServiceNow itself is living in the “commit economy”

ServiceNow disclosed $4.7B in non-cancellable cloud services obligations — and $2.8B of that sits in 2030.

Even at $15B+ scale, ServiceNow isn’t just selling through hyperscalers — they’re also a massive, long-dated buyer in the same commit economy.

And the spike in 2030 shows how multi-year cloud commitments concentrate.

5️⃣ Their “platform pitch” is really an ecosystem pitch

CEO Bill McDermott: “AI doesn’t replace enterprise orchestration. It depends on it.”

AI isn’t eating the enterprise platform. It’s eating “feature” vendors.

Real value happens when models are built into workflows where real decisions are made.

His definition of a modern platform is not “we have AI.” It’s: the platform has to work with language models, hyperscalers, data lakes, and systems of record — and stitch them into something coherent.

For alliance leaders, that’s a strong signal that the ecosystem is becoming part of the product.

Partnering with all the power centers at once

ServiceNow expanded partnerships they called out this quarter include Microsoft, OpenAI, Anthropic, NTT DATA — and they explicitly highlight relationships with Amazon Web Services, Google Cloud, Microsoft Azure, and NVIDIA.

Question for alliance leaders:

In your GTM, are partners and hyperscalers still ‘supporting’… or are they becoming the operating system for growth?

Co-Sell Challenge: Why Your Pitch Gets Ignored

Cloud account managers at AWS, Azure, and Google carry quotas that would make most CEOs sweat - often $100M+ a year.

When you ask for their time, you’re competing against hundreds of partners and thousands of accounts.

Ask yourself: If you had a $50–100M quota, how much time would you spend on a pitch with an unclear benefit?

That’s not cynicism—it’s math. And it explains why most first co-sell calls go nowhere.

What actually works: the 5-Minute Intro

The formula: Customer outcome → Cloud outcome (specific services) → Your outcome.

What’s your one-liner use case?

Skip features and jargon. Focus on customers.

“We reduce <metric> by <X%> in <N> weeks for <buyer persona>.”

“In <industry/geo>, we delivered <ROI/time-to-value>. Two recent examples: <1> and <2>”

Why should a seller care?

Translate how this makes the cloud provider win and tie it to consumption.

Does it drive new workloads? New line of business? Expansion of specific services? Helps with their AI story? Be explicit about their benefit, not yours.

“Workloads run on <Service>. Deal drives < e.g. AWS Bedrock> usage and <> hours.”

Emphasize that you transact through the marketplace - tied to their comp, helps customers burn commits, etc.

Who is your sponsor at this customer?

Prove you’ve done the work - already have traction in the customer and aren’t fishing.

What have you already done?

Champion mapped. Security review complete. Buyer path aligned to marketplace workflows.

What’s your ONE ask?

Account intel? Customer’s spend commitment? Help with POC? Procurement intro?

One ask per touch. Many asks = no action

3 principles that make this stick

About-YOU, not about-me

Swap features for customer and cloud benefits. Refine to 2–3 short sentences.

Narrow scope

Start with one deal + one vertical + one region + one repeatable use case. Don’t boil the ocean.

Right pitch, right room

AEs care about revenue and speed. Engineers care about fit and risk. Procurement cares about time and terms. Keep the outcome constant; adjust the angle.

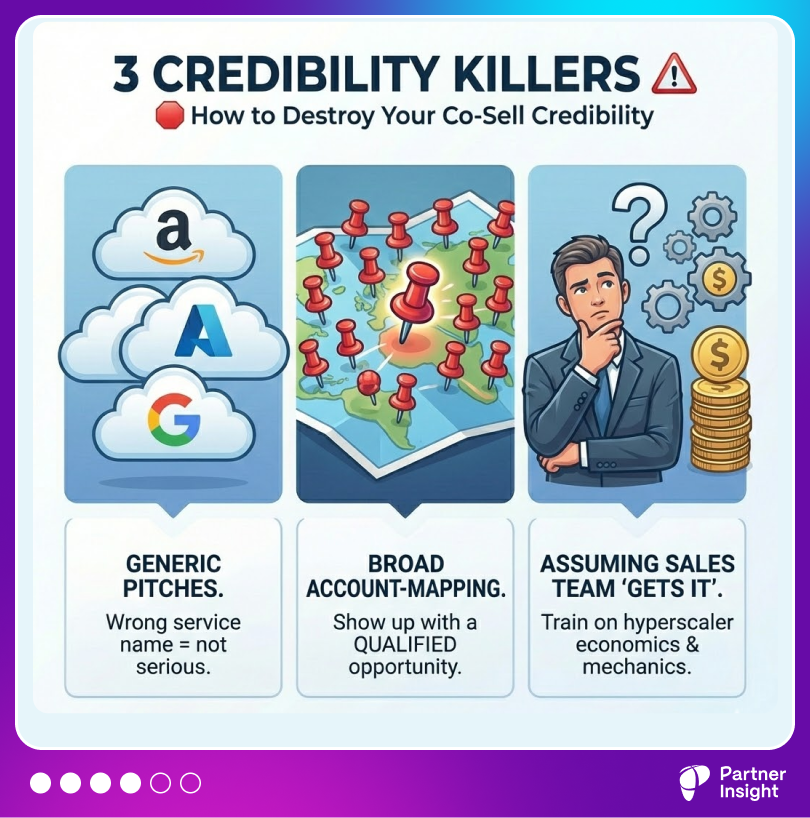

What kills your credibility

Generic pitches across clouds

Say the wrong service name and you’ve signaled you’re not serious.

Broad account-mapping sessions

Unless you’ve already closed together, sellers won’t spend hours theorizing. Show up with a qualified opportunity.

Assuming your sales team “gets it” instinctively

Even seasoned enterprise reps need training on hyperscaler economics and marketplace mechanics, if they don’t have previous cloud experience.

Most successful alliance leaders personally join the first seller calls to frame and de-risk the conversation. Then they hand-hold the first five to ten wins.

What’s your co-sell process?

Want to be featured in Partner Insight? Join our Contributor Circle

Each week this Partner Insight newsletter reaches 5,000+ Cloud GTM leaders.

I’m opening a small Partner Insight Contributor Circle for senior operators in Cloud GTM / Alliances / Marketplaces who are willing to share their practical playbook or case study this quarter.

I’m looking for operator field notes — the playbook you used, the metrics that moved, the template that saved hours.

Get featured across Partner Insight newsletter and LinkedIn insight

A direct line to me + the Partner Insight network

What I’m looking for

Cloud GTM Strategy or marketplace deal breakdown

Marketplace execution playbooks: steps, metrics, timelines.

Templates you use: co-sell intros, one-pagers, checklists.

AI workflows/prompts with impact: what you automated → output → result

Interested?

Reply to this email (or email newsletter@partnerinsight.io) with:

Your name, role, LinkedIn

What you can share (2-3 sentences on why it’s compelling).

We’ll follow up shortly.

Microsoft: Azure +39%, $625B Backlog + Agents Are the New Apps

$625B. That’s Microsoft’s total commercial cloud backlog (RPO) this quarter (+110% YoY).

Yes, OpenAI is a big chunk — but even excluding it, the commitments still grew 28%.

Cloud momentum in addition to the mega-deals

CFO Amy Hood said ~45% of total RPO is driven by OpenAI. The remaining ~$345B (+28%) reflects what she called “ongoing broad customer demand across the portfolio.”

Azure itself grew impressive 39% YoY, beating guidance.

Microsoft Cloud revenue crossed $51.5B this quarter. Using my previous conservative 45% Azure share proxy, that implies ~$90B+ Azure revenue annualized.

But Azure growth could have been even higher. With demand still exceeding capacity, Microsoft is rationing compute across M365 Copilot, GitHub Copilot, R&D, Teams, and Azure.

Satya Nadella was clear on the strategy: “We don’t want to maximize just one business... [we want to] build the best LTV portfolio.”

Amy Hood noted that if the GPUs that came online were allocated entirely to Azure, growth would have been “over 40.”

The bigger strategic play: agents as the next platform

Satya suggested to “[think of] agents as the new apps” and laid out the full stack requirements: model catalog, tuning, orchestration, context engineering, safety, observability, and security.

Side note (maybe I’m biased): that stack description reads a lot like what marketplaces do at scale — catalog + distribution + governance + trust — just applied to agents.

Agent adoption is already meaningful:

Over 80% of Fortune 500 companies have active agents built using Microsoft’s low-code tools.

M365 Copilot hit 15 million paid seats, with seat adds up 160% YoY.

Larger deployments are accelerating — the number of customers with 35,000+ seats tripled, including one deployment at 95,000 seats.

The control-plane move is particularly interesting.

Microsoft introduced Agent 365 to extend governance, identity, and security controls to agents — even those running on other clouds.

Adobe, Databricks, SAP, ServiceNow, and Workday are already integrating.

As Satya framed it: “We are the first provider to offer this type of agent control plane across clouds.”

Governance is scaling alongside AI adoption

One datapoint shows the governance layer is growing with usage: 24B Copilot interactions audited by Purview (+9x YoY).

This signals where enterprise AI spending will increasingly concentrate: not just model access, but compliance, auditability, and risk management tooling.

AI infrastructure buildout is remarkable

Microsoft spent $37.5B on CapEx this quarter. That’s ~$150B annualized pace if continued — though management expects CapEx to step down sequentially next quarter.

Still, Microsoft is compounding two engines at once: strong cloud growth and a rapidly expanding infrastructure layer.

This accelerates its ecosystem — more production workloads, more partner attach, more marketplace motion.

Are you leveraging it?

Biggest AI TAM shift: IT budgets to Operating Spend (+ Partner Upside)

Software captures 1% of US GDP. White-collar payroll is 20% - that gap explains why the world’s largest VC, a16z raised $15B and now all-in on AI.

But what does this mean for partners?

Andreessen Horowitz put it plainly:

AI isn’t just expanding the SaaS market — it’s now benchmarked with a much larger spend pool: labor.

New TAM math is staggering:

Even if most AI value flows to customers (a16z rule of thumb is 90% of software-driven value goes to customers, 10% to vendors), 10% of a market that’s 20X larger is still enormous.

You’ve probably heard what makes this cycle different

AI adoption spreads >5X faster

Costs collapse as model capabilities ~2X every 7 months

Infrastructure buildout is being funded primarily by hyperscalers spending ~$400B annually on AI capex. They bear the burden — and, as a result, they also become the gravity wells for ecosystems where partners capture value.

Here’s the part that matters most:

New rules of software

1️⃣ Systems of action will matter more than systems of record

Software that only stores data becomes less compelling. The new moat is agentic capability layered on top of workflows — software that can do the work, not just track it.

As we move from systems of record to systems of action, the winners won’t be the ones that help store the truth — they’ll help execute it.

2️⃣ Defensibility becomes operational

Models will swap out via API. What doesn’t swap easily is everything around them: integrations, rules, approvals, security, governance, and trust. Stickiness shifts from UI to embedded process.

3️⃣ Pricing shifts from seats to outcomes

Seat-based pricing starts to break when software replaces tasks. The direction of travel is clear: buyers want to pay for value created, not the number of logins.

What this means for partners + Cloud GTM leaders

The partner ecosystem becomes the moat — because the bottleneck is change

Bottleneck isn’t an AI model choice. It’s org change: data readiness, workflow redesign, governance, security, and adoption.

Models are swapping out via API. What doesn’t swap easily is change management. That’s why partners become the moat.

Trust + access become GTM advantages

In an agentic world, “who can run in production” matters more than “who demos best.” Partners who can deliver safe rollout, controls, and proof become power brokers.

Marketplaces become the rails for outcome buying + governance

If significantly more software is built and used by more people, more often, companies will desperately need rails to evaluate, buy, govern, expand, and measure.

Marketplaces help to experiment safely and turn into repeatable purchase — with packaging, commits, and expansion built in.

They will be a governance layer for agentic software: approved vendor, billing, terms, and usage controls in one place.

Net:

Software market may feel threatened — but the bigger story is software moving into work, expanding the pie, and creating a new layer of value.

What’s your take?

P.S. Thanks for reading! If this issue sparked an idea, please forward it to your alliance lead or cloud counterpart — it’s how this community shares what works.

P.P. S. Have a killer playbook like the Co-Sell guide above? Check our Contributor program above to get featured.