$2.52T AI Spend in 2026: 3 Growth Drivers + Marketplace Playbook

Hi, it’s Roman Kirsanov from Partner Insight newsletter, where I deconstruct winning Cloud GTM strategies and the latest trends in cloud marketplaces.

In today’s newsletter:

AI spend jumps to $2.52T in 2026 (up from $1.76T in 2025) — and the real signal is where the money moves: $401B more into infrastructure + $149B into AI services (what this Gartner forecast means for your partner stack).

Seller adoption of marketplaces isn’t a “motivation” problem — it’s incentives + enablement + measurement (5 field-tested levers to drive seller behavior and scale Marketplace-driven revenue).

Tech services are getting squeezed and expanded at the same time — McKinsey flags 20–30% compression in “manual” services while agentic AI creates up to $400B of new ecosystem opportunity by 2030.

Cohort 14 of our Cloud GTM Leader course just kicked off — and it’s a signal of where Cloud GTM is headed: teams are shifting marketplaces from an “end-of-quarter scramble” to a cross-functional growth system.

Before we dive in — if you’re not a subscriber yet, subscribe (free). And if this issue is useful, please forward this newsletter to your alliance lead or cloud/GTM counterpart — it’s how this community shares what works.

AI Spend to Hit $2.52T: 3 Growth Drivers in 2026

AI spend is projected to jump from $1.76T (2025) to $2.52T (2026). The number is big. But the shape of the growth is what matters.

I rebuilt the Gartner forecast into a 2025 → 2026 view, and three things stand out for alliance leaders.

1️⃣ Services is the most interesting signal: AI adoption is becoming partner-led at scale

AI Services is the #3 biggest absolute growth bucket — adding $149B in 2026 alone.

That’s Gartner highlighting what most operators already feel:

AI success is less about a “feature launch” and more about implementation — integration, governance, security reviews, data readiness, change management, and ongoing optimization.

This is where partners win.

SIs/MSPs aren’t an add-on. They’re the adoption engine that makes AI usable inside real companies.

If you lead alliances, this should inform your partner strategy: your “AI partner stack” is becoming a repeatable delivery motion.

2️⃣ Gartner’s bigger message on SaaS: incumbents have a winning path — if they prove outcomes

There’s a loud narrative that “SaaS is disrupted by AI.” Gartner pushes back:

“Because AI is in the Trough of Disillusionment throughout 2026, it will most often be sold… by their incumbent software provider…”

In plain language: buyers still prefer familiar vendors — but only when ROI is defensible.

My view: both outcomes will likely happen.

Some legacy software companies will accelerate (distribution, budgets, procurement paths, installed base).

Others will get disrupted (if they can’t ship real outcomes, or AI collapses differentiation).

The key takeaway: the default outcome isn’t “SaaS dies.” It’s “SaaS gets re-ranked by outcomes.”

3️⃣ Infrastructure is the gravity — turning cloud into the distribution layer for everything else

Infra shows the biggest dollar increase. Gartner calls out providers “building out AI foundations,” with infrastructure adding $401B in 2026.

When infrastructure becomes the largest and fast-expanding pool, the cloud becomes the distribution layer for everything else — software procurement, services delivery, and the operating model around it.

If you’re not aligned to hyperscaler motions, you’re not aligned with the strongest pull.

Fastest % growth (small bases, loud signals):

AI Data grows ~3x (data readiness is key)

AI Cybersecurity nearly doubles (governance and risk budgets are catching up fast)

AI Models also grow quickly, though from a smaller base than infra/software/services.

What this means for marketplaces

Put those signals together and the implication is clear. If the fastest-growing spend pools are infrastructure + software + services, the winners will be the companies that can:

attach to hyperscaler infrastructure budgets (cloud consumption, committed spend, procurement convenience),

sell AI software as an expansion of existing buying paths (like marketplaces)

and package services so adoption doesn’t stall after purchase

PS. Source

5 Seller Incentives To Drive Marketplace Revenue

Marketplace adoption by field sales teams is not a “motivation” problem. It’s an “incentives + enablement + measurement” problem.

Marketplace is one of the few GTM levers that can materially change outcomes — bigger deals, faster closes and less procurement friction. Yet many field sellers are slow to adopt them.

Recently we discussed how to drive Marketplace adoption & revenue in a webinar with AWS + ISV leaders.

Here are 5 incentives they see working:

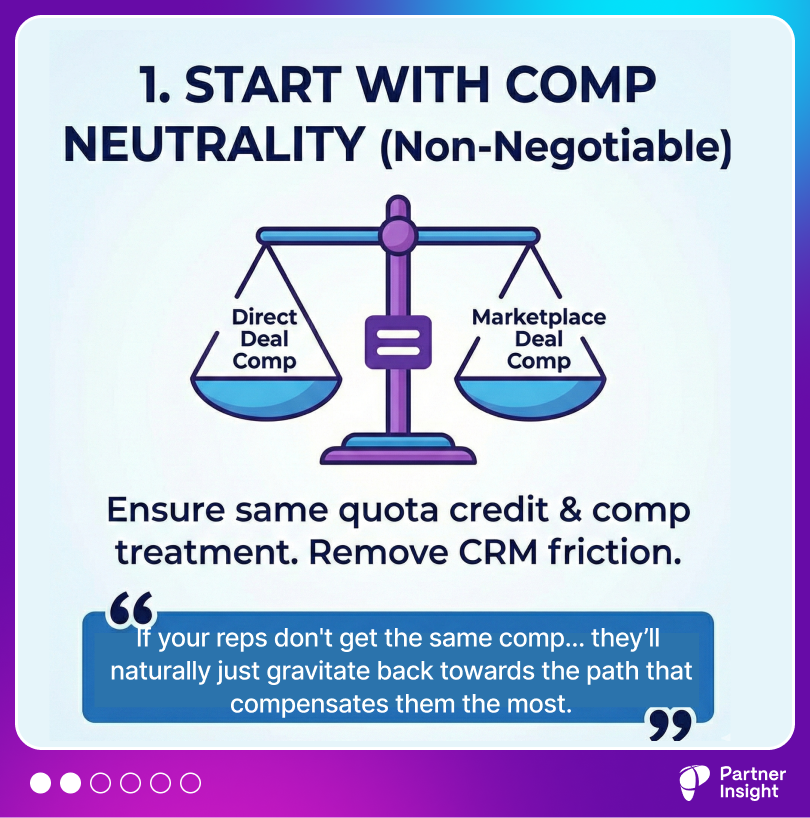

1️⃣ Start with comp neutrality

Juston Salcido (then Sr. Partner Development Specialist at AWS) put it plainly:

“If your reps don’t get the same comp for deals that go through Marketplace that go direct, they’re gonna naturally just gravitate back towards the path that compensates them the most.”

Translation: Marketplaces need the same comp treatment + integrated into the sales process/CRM, not bolted on at the end.

2️⃣ Run a temporary comp-positive SPIF (to drive behavior change)

Comp neutrality removes the penalty. SPIFs create momentum.

In practice: time-box it (6–12 months), trigger when deals are transacted via Marketplace, and tier it by deal size so you’re not overpaying on small deals.

Kyle Heisner (Head of GTM & Alliances, Suger) shared what happens when a company removed it too early:

“He dropped his SPIF program… and he saw a 40% drop in the next quarter… [and] immediately went back and implemented it.”

3️⃣ Add recognition + competition

Prashant Pai (EVP, Strategic Alliances, KnowBe4) explained how they reinforce behavior at scale:

“We have an internal leaderboard… and we share that all the time on our revenue cadence calls. These reps have done the most deals through marketplaces, these reps have done the largest deals… We do that for our direct sellers, for our renewal folks, and for our channel folks as well.”

This works because sellers are competitive — and it makes Marketplace visible inside the revenue org.

4️⃣ Pay sellers to become internal evangelists

Mike Marzano (Global Head of Cloud Alliances, Contentsquare) described my favorite “second-order” incentive he implemented for his field:

“By going through the marketplace, you’ll get a SPIF. But if you go and put a story out on our global sales channel about why you co-sold, how you did it… what went well… what you’d do better… and you share that out… I’ll pay you more.”

That’s how you turn one win into a shared playbook.

5️⃣ Make Marketplace measurable

Juston’s conclusion was simple:

“You really gotta start tracking… the average deal size for direct deals, the average deal size for deals that go through Marketplace and have a co-sell influence.”

This helps sellers see faster cycles / bigger deals, Finance (and the rest) to see time-to-cash, and why Marketplace fees are worth it.

If you don’t measure it, the program becomes opinion — and may get cut when priorities shift.

AI Reshapes Tech Services as Outsourced IT Spend Set to Rise (McKinsey)

Traditional IT budgets are tightening, yet agentic AI and outsourcing spending 📈 are expanding. How do you square that circle?

Let’s look at the tech service market, where partnerships are now crucial and compression and expansion happen at the same time.

McKinsey & Company frames the shift as we move from creating code to agentic AI—software that can take actions across systems.

Rules for service providers, SIs, ISVs and hyperscalers are changing.

⬇️ Where the market is compressing

A lot of work that used to justify headcount or long service engagements is getting cheaper:

routine execution is increasingly automated

more teams are building capability in-house

repeatable delivery is harder to price by the hour

Pure-play AI startups and platform providers will sometimes go direct, bypassing parts of the traditional SI motion.

McKinsey estimates this could contract parts of traditional Tech Services by 20–30%. Services aren’t dying — but services tied to manual execution face the most pressure.

⬆️ Where the market is expanding

At the same time, scaling agents creates new spend. McKinsey estimates $100B–$400B of incremental opportunity by 2030, including:

Workflow services ($200B): designing the architecture, governance, and security for agents. Making agents work in the enterprise requires complex integrations, permissions, monitoring, and exception handling—problems most teams can’t solve alone.

Business function transformation: redesigning how departments (HR, support, ops) run with “human + agent” workflows.

Partnerships and ecosystems matter more than ever

Historically, companies scaled first, then partnered. In the agentic era, many will need to partner before scale to offer a complete solution.

No single vendor delivers end-to-end agentic AI. Real deployments demand a best-of-breed mesh across models, orchestration layers, SaaS platforms, data, and security. In practice, the fastest path to production is usually an ecosystem play—not a single-vendor promise.

That shifts market dynamics:

Service providers increasingly productize delivery (“service-as-software”) by building reusable IP, not just selling hours.

Marketplaces matter more as packaging and procurement rails for repeatable solutions—especially when integrations and controls are proven.

Hyperscalers are foundational, but partnerships become less about resale mechanics and more about deep technical integration and shared delivery patterns.

What winners tend to do

Winners won’t be the broad generalists. They’ll be specialized builders who:

bring real domain expertise (you can’t build a healthcare claims agent without claims expertise)

align pricing to outcomes

treat ecosystem readiness as a first-class product requirement, not a late-stage GTM add-on

The market is adjusting for those who sell effort. It’s expanding for those who can reliably deliver outcomes.

PS. Source

Insights from Cloud GTM Leader Cohort 14 launch

Cohort 14 of our Cloud GTM Leader course just kicked off — and what stood out was the cross-section of partner operators being pulled into marketplaces from different directions inside the partner org. This tells you where Cloud GTM is going next.

Leaders who run partner sales, partner ops, regional channels, and teams building the alliance motion from zero all shared the same conclusion:

Marketplace GTM may start in alliances, but it’s too strategic and too consequential for revenue, so it scales through the cross-company efforts.

They’re converging on the same problem: turning the marketplace from an end-of-quarter scramble into the default buying path. For some it’s about learning; for others it’s about scaling; for a few experienced operators it’s also about giving back.

Here are 5 signals you can learn from:

1️⃣ Marketplace is no longer a “nice to have”

Multiple leaders said customers, partners and field teams have shifted from being curious about marketplace… to actively demanding it.

2️⃣ Private offers are driving most of the value

One mature operator shared their early thesis was “public offers + product-led.”

What actually moved (massive) revenue: private offers + repeatable co-sell motions.

And the pressure is now coming from the field: where marketplace flows exist, sellers want them; where they don’t, they complain.

3️⃣ The biggest bottleneck is still internal

A consistent pattern came up across roles: the cloud side is workable… but internal alignment often takes months.

Comp neutrality was mentioned repeatedly as the hinge point — without it, marketplace becomes “special handling,” and AEs avoid it. Several described extended internal evangelism just to get a reliable “yes” from Sales leadership.

4️⃣ Global + multi-cloud scaling isn’t copy/paste

Leaders working across hyperscalers highlighted how different each hyperscaler motion feels. You need to learn and adapt substantially.

It’s equally hard to replicate one-geo success across the full GTM org. In some markets you can’t even go direct; distribution structures and local rules can change the strategy.

5️⃣ Marketplace is becoming a cross-functional operating system

This isn’t just about listing. It touches comp models/incentives, deal desk, billing, product packaging, approvals, and CRM integration. That’s why partner ops and revenue plumbing are increasingly part of the conversation.

Net takeaway:

In 2026 Cloud GTM isn’t just “doing marketplace.”

It’s designing and implementing a scalable system where marketplace is an easy path for your buyers and sellers to transact — and it’s embedded operationally, financially, and culturally across the org.

Enterprise budgets, C-suite priorities, and hyperscaler focus are all tilting toward marketplaces. When buyers prefer to buy this way, companies and sellers follow the money.

Cohort 14 of Cloud GTM Leader course will be a deep dive into building that system. Excited to learn together over the next five weeks with 15+ incredible operators.

P.S. If you found these insights valuable, please forward this newsletter to your alliance lead or cloud/GTM counterpart - it’s how this community shares what works.

Hey Roman, great read as always. Your breakdown of where the AI money is really going makes so much sence. The idea of agentic AI creating new opportunities is especially exciting to me, like imagining my future AI assistant finally sorting my books by color and publication year.