90% Channel. 50% Co-Sell. Inside Dynatrace's $1B Marketplace Playbook

Hi, it’s Roman Kirsanov from the Partner Insight newsletter, where I deconstruct winning Cloud GTM strategies and the latest trends in cloud marketplaces.

In today’s newsletter:

Dynatrace crossed $1B in AWS Marketplace sales — with ~90% channel transactions and 50%+ co-sell across all three clouds. The alliance playbook behind it is what matters.

Who actually sources Marketplace deals? IDC data shows ISV AEs open 45% of opportunities — yet sellers who co-sell report 2X sales growth. Why the gap is the strategy.

Speaker reveal: Drew Zurek (ex-AWS, trained hundreds of CROs on marketplace sales; now leads marketplaces at Qlik) joins our free Feb 24 workshop to share how top ISVs activate sellers to scale marketplace revenue.

Partnerships hit board level: 79% of CEOs plan strategic alliances in 2026, up from 62% in 2025 — because transformation can’t wait and AI capability gaps are forcing ecosystem bets.

Before we dive in:

The pattern is clear: marketplace winners aren’t waiting for hyperscalers to source deals—they’re building the internal muscle to convert pipeline with them.

That’s exactly what we’ll break down on Feb 24 (9–10am PT) in a free, tactical workshop: seller activation frameworks, CRO/CFO alignment, comp design, and 5 templates you can implement this quarter—led by operators who’ve done it at AWS and at scale.

Inside Dynatrace’s GTM: 90% Channel, 50% Cloud Co-Sell

90% of transactions through partners. 50%+ co-selling with all three hyperscalers.

That’s the GTM playbook behind Dynatrace’s $1B AWS Marketplace milestone - and one that alliance leaders should study.

Dynatrace just crossed $1B in lifetime AWS Marketplace sales, with triple-digit marketplace growth still accelerating.

The company beat guidance across every metric last quarter, raised its full-year outlook, and is about to cross $2B ARR.

But the milestone isn’t the story. The playbook behind it is.

Dynatrace has built one of the most partner-centric GTM strategies. 50%+ of new logos were partner-originated in a recent quarter. The company has passed 50% co-sell with all three hyperscalers.

Today, partners aren’t optional

CEO Rick McConnell stressed in a recent earnings call:

“In an agentic world, engaging in and integrating with an ecosystem of partners, including global system integrators and hyperscalers, will be mandatory. And we are investing to deepen and broaden those relationships.”

Jay Snyder, SVP of Partners & Alliances, laid out the strategy:

“As the company has now close to 90 percent of transactions through the channel… our goal is about 75 percent of our business be co-sell, and a good portion of that be through the marketplace.” (CRN)

Dynatrace isn’t just co-selling — it deeply integrates with all three clouds.

CEO: “In Q3, we announced deeper technical engagements with all of the major hyperscalers.

We’re integrating with Amazon Bedrock Agent Core, embedding Dynatrace with Azure’s SRE agent, and serving as the launch partner for GCP Gemini command line interface extensions and Gemini Enterprise.”

Partners are a productivity multiplier

And it’s showing up in seller economics.

CFO James Benson: “We’ve continued to get significant traction with leveraging our partner channels, notably GSIs, and the hyperscalers continue to be a source of continued improvement in productivity per rep.”

Partners and hyperscalers also pull the company into deals earlier:

“By working more closely with strategic partners, our objective is to participate in digital transformation projects earlier in the purchasing cycle.”

That’s why Dynatrace is committing to “invest in our strategic partner ecosystem”.

Meanwhile, the company disclosed $702.8 million in internal cloud commits...

What alliance leaders should take from this:

Co-sell and marketplace are one motion, not two. Dynatrace didn’t build separate marketplace and co-sell plays. They run them together as one strategic GTM.

Agentic AI creates new partnership surface area. Dynatrace is embedding into each hyperscaler’s AI agent infrastructure. Every new AI integration becomes a new co-sell trigger.

Partners are a productivity multiplier. If your alliance team can’t show that math internally, you’ll keep fighting for headcount.

When partner strategy shows up in earnings calls — not just alliance decks — it’s no longer a channel play.

It’s a corporate strategy.

Speaker Reveal: Drew Zurek (ex-AWS, now Qlik) — Activating Sellers to Win Marketplace Revenue

Most ISVs agree marketplace matters. But marketplace and ecosystem revenue doesn’t scale on intent — it scales when your sales team knows how to position it, sell it, and win with it.

That’s the gap Drew Zurek has spent his career closing- first as a sales leader driving enterprise growth, then inside AWS, now as an operator at Qlik. And he’s joining our Feb 24 webinar to share exactly how.

Drew is Senior Director, Global Cloud Marketplaces at Qlik, leading marketplace and ecosystem sales and strategy for an organization serving 40,000+ customers globally (and a 15-year Gartner Magic Quadrant Leader in Analytics & BI).

What makes Drew’s insights unique for this session:

During 4 years at AWS, Drew was embedded in the partner growth machine.

He helped architect marketplace strategies for hundreds of ISVs while developing and running the CRO (Chief Revenue Officer) / Head of Sales Fellowship—hands-on sessions designed to teach revenue leaders how to operationalize and expand their co-sell relationship with AWS and Marketplace.

Those Fellowship cohorts trained hundreds of leaders to scale marketplace GTM across their sales teams and accelerate growth.

Having impacted thousands of partners, he’s seen the full spectrum: which companies turn co-sell into a revenue engine and which ones stall at the listing stage.

Now he’s executing that same methodology on the operator side at Qlik.

Drew understands the complete picture.

He knows what hyperscalers want to see from partners.

And he knows what it takes internally—leadership alignment, seller activation, comp structure, deal mechanics—to make marketplace and ecosystem sales work at scale.

That’s exactly what this online workshop is built around.

🗓️ Join us Feb 24, 9–10 AM PT as we break down:

How to structure your marketplace motion so sellers actually use it (not work around it)

The leadership alignment playbook that gets CRO and CFO buy-in

What top companies are doing differently in 2026 to scale marketplace revenue globally

Templates you can take back to your team and implement this quarter

Drew will be joined by an AWS leader, Trunal Bhanse (CEO, Clazar), Fabrizio Cataldo (Business Development & Partnerships, Supabase), and myself.

We’ll cover this from multiple angles: the key industry drivers, strategic growth patterns we’re seeing working across the market, the hyperscaler perspective, and the automation/ops layer.

If you want to learn from someone who built the playbook inside AWS, trained hundreds of CROs across the industry, and now runs it at a 40K-customer enterprise—this is the session.

Thanks to our partner Clazar for supporting this workshop

Clazar is the leading Cloud Sales Acceleration Platform for Go-to-Market teams to scale revenue on AWS, Azure, and Google cloud marketplaces. From listing to co-selling to revenue reconciliation and recognition, our platform helps companies streamline and automate their entire cloud sales journey from a single, unified platform—with zero operational overhead.

Clazar integrates seamlessly with leading CRMs, offers robust governance controls, and fully complies with industry-leading security standards. Top companies like Pinecone, Perplexity, Confluent, Cursor, and Replit trust Clazar to power their success on cloud marketplaces.

To learn more, please visit www.clazar.io

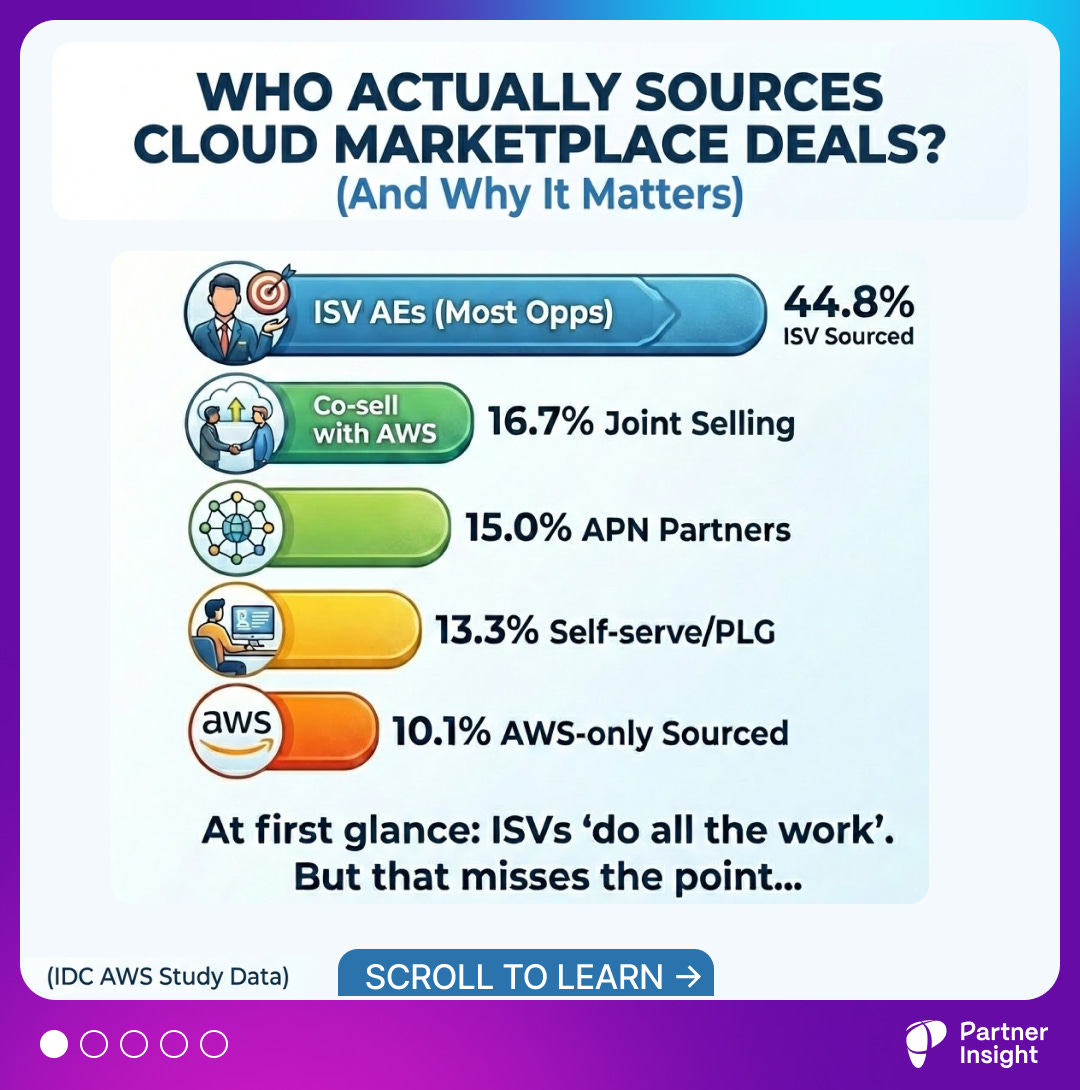

Who Actually Sources Cloud Marketplace deals?

And if hyperscalers “only” source 10–20% of deals, are Marketplace and co-sell overrated?

IDC’s recent AWS Marketplace study breaks down the numbers:

ISV AEs open most opportunities: 44.8% sourced by ISVs

Joint discovery (co-sell) with AWS: 16.7%

AWS-only sourced: 10.1%

The rest: APN partners 15.0%, self-serve/PLG 13.3%

At first glance, it looks like ISVs “do all the work” on marketplaces, while hyperscalers get the credit.

Here’s my read of the report—and why that interpretation misses what’s actually driving the 2X growth numbers.

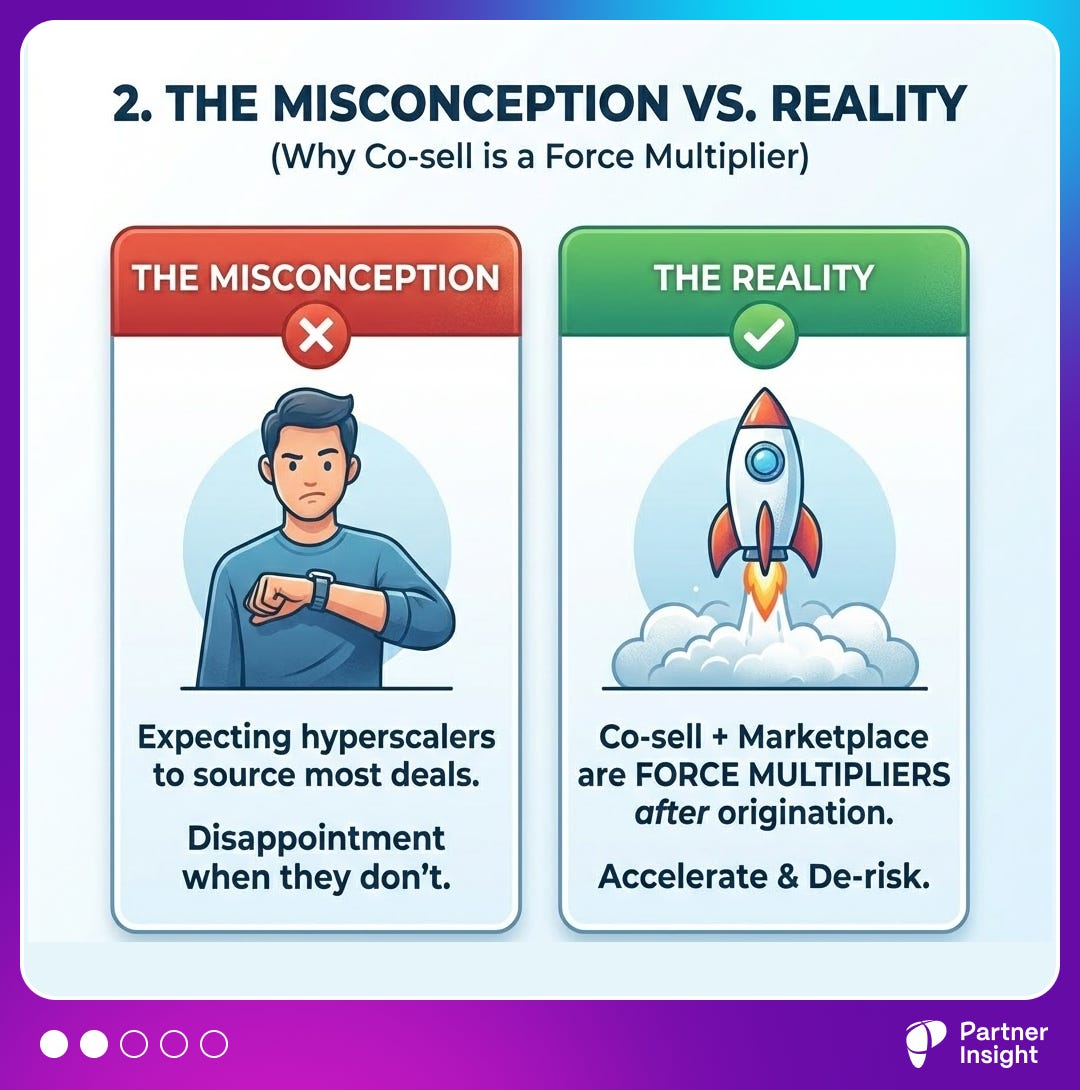

The misconception killing marketplace strategies:

Many alliance leaders list in marketplaces expecting hyperscalers to source opportunities. When they get only a handful of deals, it feels like a failed promise. But origination and co-sell are fundamentally different jobs, and confusing them leaves the biggest growth lever unused.

Reality: co-sell + Marketplace are force multipliers after origination.

Most ISV-sourced opps become co-sell later to accelerate the cycle, retire commits, and speed procurement/legal via Private Offers.

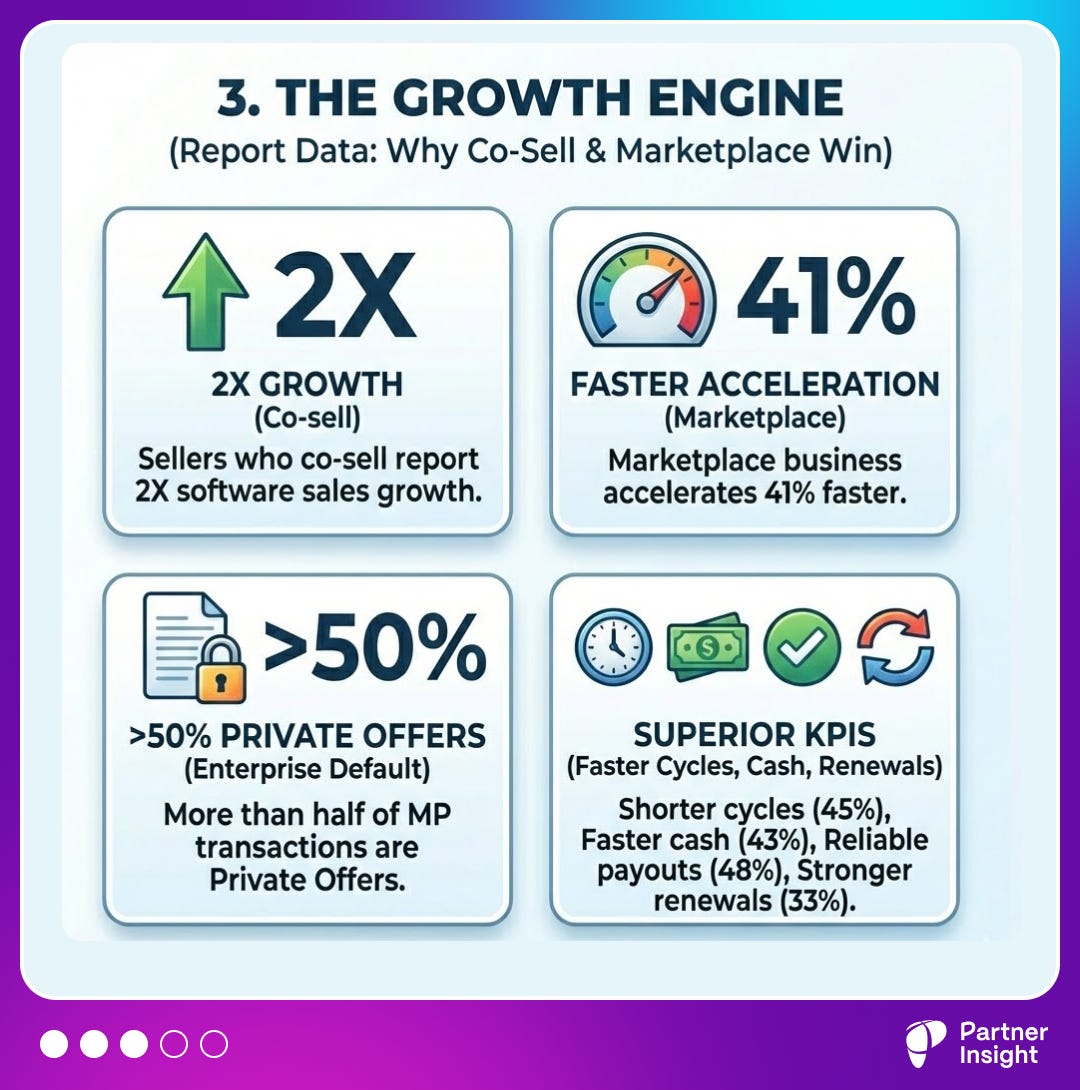

Why Co-Sell and Marketplace drive faster growth (report data)

Sellers who co-sell report 2X software sales growth vs. those who don’t.

75% of surveyed sellers co-sell with AWS and see that lift. If you’re not co-selling, you’re leaving the biggest lever unused.

Marketplace businesses accelerate 41% faster

AWS Marketplace revenue grows ~41% faster than the rest of software for surveyed sellers.

Private Offers are the enterprise default (>50% of MP transactions)

More than half of AWS MP transactions are Private Offers; over a third of sellers’ reps have executed at least one

Marketplace KPIs are superior

Sellers cite shorter cycles (45%), faster cash collection (43%), more reliable payouts (48%), and stronger renewals (33%) vs. traditional motions.

Result? 23% of revenue through MP

Companies listed 55% of their portfolios. With nearly a quarter of revenue via MP, it’s now a core driver.

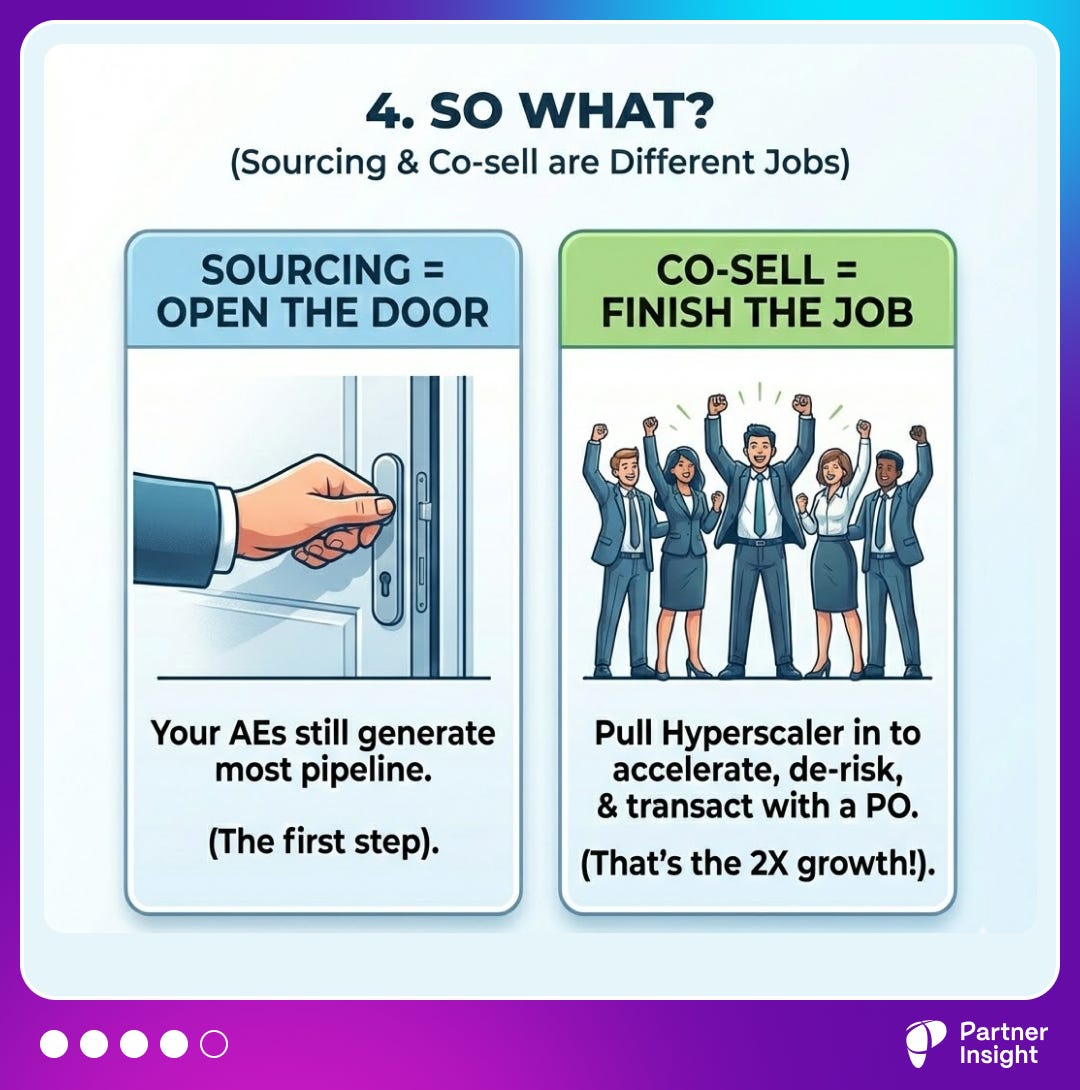

So what? Sourcing and co-sell are different jobs

Sourcing = open the door. Your AEs still generate most pipeline—by design.

Co-sell = finish the job. Pull AWS in to add account intel, credibility, learn about customer commits, get exec cover, and transact with a PO. That’s where the 2X shows up.

Yes, only ~10% of deals are sourced by hyperscalers and ~17% are jointly sourced.

Yet co-sell and Marketplace remain the growth engine because they change the outcome of the other 70% you sourced yourself.

Generate the pipeline; use AWS and MP to accelerate, de-risk, and close. That’s how companies already drive 23% of their revenue and growing.

Source: Research

Want the Marketplace Operator Playbook?

On Feb 24 (9–10am PT, online) we’ll break down how to turn cloud commits into Marketplace revenue - seller activation, CRO/CFO alignment, and templates you can implement this quarter.

79% of CEOs plan to pursue strategic alliances and JVs in 2026 — up from 62% in 2025

17% jump in a year means that partnerships are now a CEO-level transformation lever, not a side program.

That’s data from the EY-Parthenon CEO Outlook 2026 — a survey of 1,200 CEOs across 21 countries conducted in Nov–Dec 2025.

The backdrop explains the urgency

97% of companies are undergoing a significant transformation or are about to start one.

“The majority of CEOs now report that they are either in the midst of a significant enterprise-wide transformation initiative (52%) or plan to begin one in 2026 (45%).”

At the same time, “61% of CEOs anticipate higher operating costs in 2026.”

The pressure is real: transform faster while spending more carefully.

What are they optimizing for?

“Globally, 43% of CEOs identify optimizing operations and improving productivity, including digitalization, as their top desired outcome.”

40% prioritize “improving customer engagement and retention”.

It’s telling that customer retention is now higher priority than accelerating growth (36%).

Now the partnership spike makes sense

Companies need to transform, digitize, engage customers and grow faster.

79% of CEOs plan to pursue strategic alliances and JVs in 2026, up from 62% in 2025 — a “sharp rise that underscores the appeal of partnerships in unlocking access to new capabilities.”

Why? Because “these collaborations offer a pragmatic route to accelerate innovation and share risk.”

It concludes: “Alliances and JVs are emerging as critical levers for speed, flexibility, and adaptability in an environment where transformation cannot wait.”

AI technology is no longer experimental

Reflecting on AI impact, 20% of CEOs say that AI outcomes are “significantly above expectations”, and 58% “somewhat above” — 78% above expectations in total.

But scaling AI enterprise-wide requires capabilities most companies don’t have in-house.

As we discussed before, strategic alliances—whether with hyperscalers, technology vendors, or implementation partners—are becoming the default path to close that gap.

The EY data suggests we’re in a new phase: one where alliances are essential infrastructure for transformation and growth.

What’s your read—are you seeing the same urgency from your customers and partners?

Source: research.

P.S. If you found these insights valuable, please forward this newsletter to your alliance lead or cloud/GTM counterpart - it’s how this community shares what works.