AI Budgets Are Up. But CIOs Are Still Cutting Vendors

Hi, it’s Roman Kirsanov from Partner Insight newsletter, where I deconstruct winning Cloud GTM strategies and the latest trends in cloud marketplaces.

Here’s what’s inside this week:

Only 3% of CIOs expect AI to lead to more vendors — 54% are actively consolidating. What a recent CIO survey reveals about their buying patterns

AI-mature buyers are ready to spend 2X more via digital self-serve, averaging $1M deals — the exact shift pushing marketplaces and cloud GTM into the mainstream

Cohort 15 starts April 7 — the 5-week system behind marketplace motions that helped alumni go from zero to $200K revenue + $7M pipeline in 8 weeks

Before we dive in — I’m running a free Cloud GTM Quarterly Live this Thursday, April 2nd, where I’ll break down the 7 most important signals from Q1 and what alliance, marketplace, and GTM leaders should do with them in Q2. Cloud commits growth, co-sell case studies, AI distribution shifts — all of it. Save your spot below.

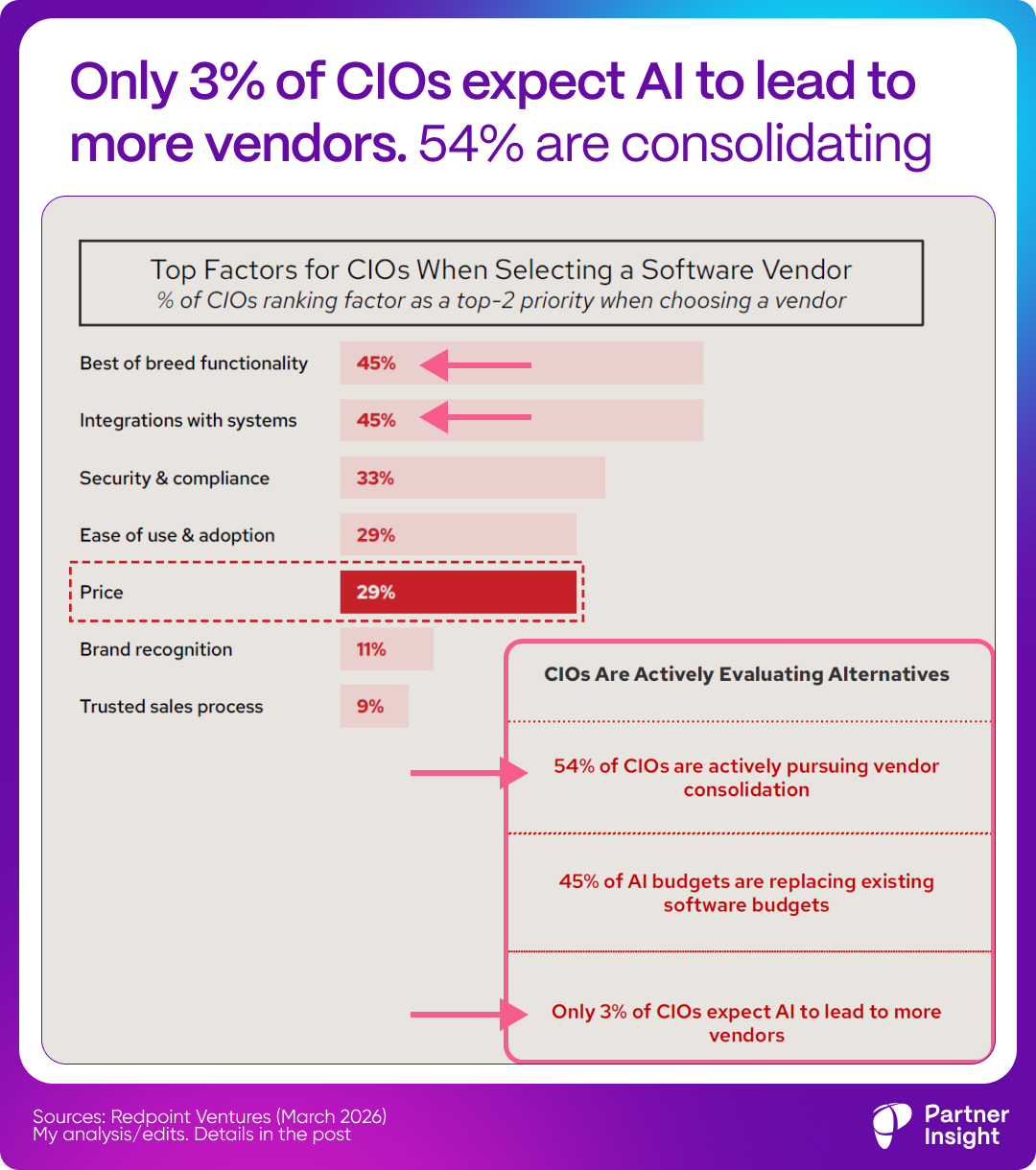

Only 3% of CIOs expect AI to lead to more vendors. 54% are consolidating

The latest CIO survey by Redpoint suggests the software battle is changing.

The hard part is no longer just getting added as a vendor. It is staying on the list at all.

Five insights stood out to me from Redpoint Ventures’ recent market update and its CIO Software & AI Survey (March 2026):

1. Incumbents have an edge — but not a lock

58% of CIOs said AI feature additions are the main reason software budgets are growing — the highest of any category.

54% of CIOs prefer their existing vendors to add AI over switching to AI-native alternatives

But look deeper:

Only 17% have a strong preference for incumbents adding AI.

37% have only a slight preference.

And 33% are neutral.

So install base still matters. But weak products without AI capabilities are not protected.

2. Vendor consolidation is not slowing down. It may accelerate.

54% of CIOs are actively pursuing vendor consolidation.

45% of AI budgets are replacing existing software budgets.

Only 3% expect AI to lead to more vendors.

AI is not opening unlimited new budget lines. In many cases, it is forcing a re-ranking of who deserves to stay in the stack.

3. Buyers still care more about best-of-breed products and integrations than price

When CIOs rank what matters most in vendor selection (after AI), they need:

45% best-of-breed functionality

45% integrations

33% security/compliance

vs. 29% price

Trusted sales process is at a mere 9%

The bar is not just “has AI.” The bar is “works inside my environment and is worth the risk.”

Meanwhile, the cloud layer keeps getting bigger.

4. AWS, GCP and Microsoft capex jumped from $211B in 2024 to an estimated $509B in 2026

Google’s 2024–2027E CAGR is shown at 49%

Microsoft’s at 33%

Amazon’s at 22%

My takeaway: more AI infrastructure spend creates more room for partner-led consumption, co-sell motions, and ecosystem pull-through. The cloud partner opportunity isn’t shrinking. It’s expanding — driven by AI workloads.

5. The real TAM shift: from software to labor

Redpoint’s agent maturity curve suggests we are moving from copilots toward task agents. That is a bigger shift than adding AI features into existing apps.

Once AI starts completing tasks end-to-end with human oversight, the addressable market moves beyond software spend and into labor spend.

Redpoint estimates that Task Agents alone expand the addressable market from ~$0.5T (US software) to $1.2T.

For cloud alliance and marketplace leaders, I take away 3 lessons:

Your AI roadmap is now your retention and growth strategies. CIOs will stay with incumbents — but only if AI delivery is real

Consolidation pressure means the winners will be partners embedded in strategic platforms, including cloud marketplaces

Pricing models are shifting: 46% of CIOs expect usage- or outcome-based pricing to become more common. 29% say seat-based pricing will decline. This maps directly to cloud marketplace economics.

What’s your strategy?

Cloud GTM Quarterly Live: 7 Insights & Playbooks to Win Q2

Every quarter I analyze company data, hyperscaler updates, marketplace trends, co-sell patterns, and what we’re seeing across our events and Cloud GTM community.

Q1 was one of the more interesting quarters — a lot accelerated at once.

Cloud commits keep climbing (~$900B across the three hyperscalers). The budget conversation is shifting from “should we buy through marketplace” to “how fast can we execute.”

The companies growing fastest are integrating Cloud GTM deeper across sales and partner teams. And AI is now changing how software gets distributed, how deals get structured, and how co-sell works on all three clouds.

I’m running a free live briefing this Thursday to walk through all of it.

I’ll share the most important signals from Q1 — from market moves, top-performing companies, and hyperscaler shifts — and what alliance, marketplace, and GTM leaders should actually do with them in Q2.

We’ll cover:

7 signals from Q1 shaping Q2 priorities across AWS, Microsoft, and GCP

What’s actually working in co-sell — and where friction is increasing

Cloud commits tracker: where budget is moving

How AI is changing distribution and GTM on marketplaces

Operator patterns separating teams that are scaling from teams that aren’t

This session leads into Cohort 15 of Cloud GTM Leader course starting April 7.

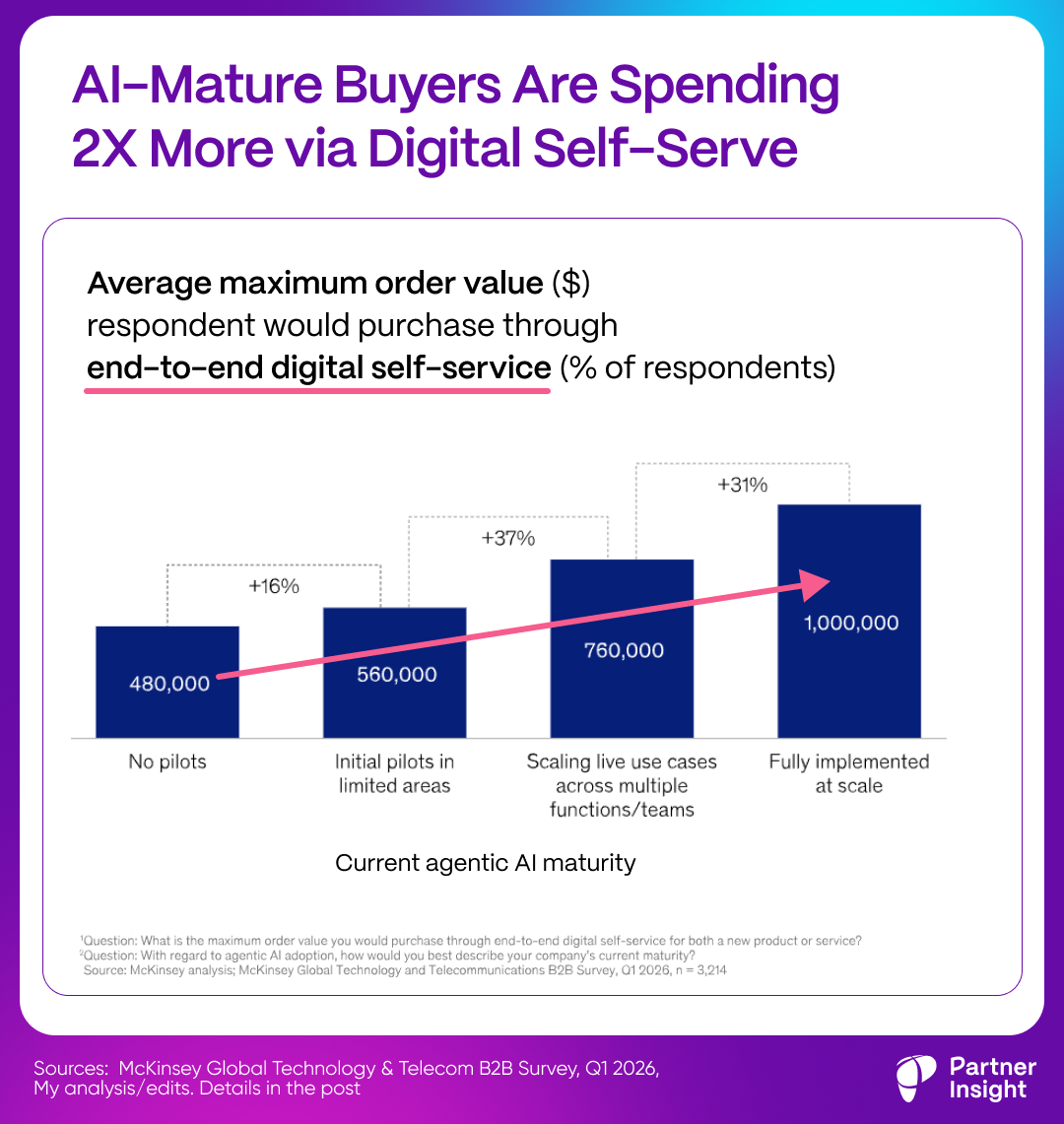

AI-Mature Buyers Are Spending 2X More via Digital Self-Serve

AI-forward buyers are driving digital spend according to McKinsey. The most AI-mature group is ready to transact $1M+ deals through end-to-end digital self-serve.

McKinsey & Company’s latest B2B survey of 3,000+ decision-makers across 18 countries points to a shift that cloud alliance, marketplace, and GTM leaders should take seriously.

As customers mature with agentic AI, they buy digitally, buy larger, and move faster with less human mediation.

Digital is no longer just a convenience layer. McKinsey calls it a shift toward a “primary growth engine.”

Here is what stood out:

1. AI maturity changes deal size

The most AI-mature buyers are willing to transact more than $1M through fully digital, end-to-end channels. That is roughly 2X the level of peers still in early pilots.

Each step up in AI maturity is linked to a 20–45% increase in the value customers are willing to buy digitally. This is not a one-off jump. It is a compounding shift in behavior.

2. Buying behavior is changing, not just channel preference

Agentic AI is reducing reliance on human-mediated interactions and increasing comfort with automated, end-to-end digital journeys.

AI is not only changing what companies buy. It is changing how they buy.

3. Human support still matters

About one-third of B2B customers expect digital-first interactions over the next 12 months. But nearly 60% still prefer hybrid models that combine digital and remote human interaction.

The winners will not be self-serve only. They will make digital easy, then bring in the right human support at the right moment.

4. Demand is moving faster than execution

Roughly 80% of large and mid-size enterprises already have agentic AI in some form. Fully implemented deployments are expected to grow 2.3–2.4X in the next 12–18 months.

But only 3–11% have reached full scale in any individual use case. That gap creates room for partners, SIs, and AI-native vendors that can help customers move from pilots to repeatable deployment.

5. Buyers want to buy AI, not build it

Across use cases, roughly 80% of B2B customers prefer off-the-shelf solutions, managed services, or third-party custom builds over building internally.

And no provider type has clearly won yet. That makes this market more open than many people think.

A few lessons for alliance and GTM leaders:

Treat digital buying as a core GTM capability, not a secondary channel

Design hybrid journeys where sales, partners, and digital channels work together

Lead with trust, packaging, and frictionless execution — security is now the #1 reason enterprises switch providers

Cloud marketplaces sit inside this shift, but the lesson is broader: AI is training enterprise buyers to spend more through digital channels. The companies that make buying easier now will have the edge later.

What’s changing in how buyers purchase your solutions?

Cohort 15 Starts April 7: Turn Marketplace Into a Real Growth Driver in 2026

Enterprises have committed $900B+ to AWS, Microsoft, and Google Cloud — budgets you can tap into via cloud marketplaces. For SaaS and AI companies, Cloud GTM is no longer optional. It is becoming a core lever for revenue growth, faster sales cycles, and easier enterprise procurement.

The most advanced GTM teams – from scaleups to public companies – are rewriting the rules. They’re using marketplaces and co-sell to scale revenue faster, compress sales cycles by 40-60%, and make buying frictionless.

Real results from real companies

Over the past 2.5 years, 300+ alliance leaders have completed Cloud GTM Leader course and built this capability. Examples of what alumni have achieved:

Launched from zero marketplace motion to $200K revenue + $7M pipeline in 8 weeks

Closed their first $1M+ marketplace deal and turned it into a repeatable motion

Scaled marketplace revenue 4X YoY from an already high eight-figure base

These aren’t outliers. They’re alliance leaders who invested 5 weeks to master the frameworks, tactics, and relationships that drive cloud GTM success.

What we master in 5 weeks:

How to tap into cloud commits + marketplace buying processes

Co-sell patterns with hyperscaler field teams that actually create pipeline

How to position on marketplaces so sellers choose you among thousands of vendors

Frameworks to align sales, product, finance, and ops around one cloud GTM plan

How to accelerate deals with smart co-marketing (and more)

If you want marketplace to become a real growth driver in 2026, join Cohort 15 starting April 7.

What alumni are saying

“I wish I had this knowledge before I started my role in the GTM department last year.”

“As someone who has built AWS alliances twice, driven marketplace success, and led cross-functional GTM motions, this program elevated my perspective and sharpened my thinking around cloud co-sell programs, marketplace motions, channel strategy, and scalable GTM frameworks. Highly recommend.”

P.S. If you found these insights valuable, please forward this newsletter to your alliance lead or cloud/GTM counterpart - it’s how this community shares what works

Interesting contradiction, but it makes sense—AI spending may be growing while overall vendor consolidation is still happening. Companies seem more willing to fund clear ROI, not tool sprawl.