One Chart Shows Cloud Marketplaces Going Mainstream

5 years of search data reveal one breakout moment across all 3 hyperscalers. Plus: LucidLink’s channel rebuild now driving 39% of revenue and Palo Alto’s AI-lab GTM playbook.

Hi, it’s Roman Kirsanov from Partner Insight newsletter, where I deconstruct winning Cloud GTM strategies and the latest trends in cloud marketplaces.

In this issue:

Marketplace interest hit an inflection across all 3 hyperscalers at once — 5 years of data reveal a category-level shift (and Microsoft is the biggest surprise)

LucidLink rebuilt its partner motion in 13 months — now 39% of revenue runs through channel partners, with a 45% net-new ARR target next

Palo Alto turned AI labs from feared disruptors into partners and buyers — driving 800 enterprise meetings in 6 weeks and $200M+ ARR with one frontier AI lab.

But before we dive in — join us next week at the AWS Marketplace Strategic Breakfast at AWS Summit NYC. June 17, 7:30–9:30 AM, near Javits Center. Four senior AWS Marketplace leaders will be in the room alongside leading ISV and ecosystem operators from companies like ServiceNow, scaling on Marketplace right now.

Cloud Marketplace Interest Hit an Inflection Point

Cloud marketplace interest broke out in 2025 - across all 3 hyperscalers at once.

AWS has the deepest transaction proof, but Microsoft and Google are closing the mindshare gap faster than many realize.

5 years of Google Trends data show a clear pattern

AWS Marketplace, Azure Marketplace, Google Cloud Marketplace all follow the same trajectory:

slow steady growth 2021-2024

then a sharp inflection in 2025

Search is not revenue. But when every hyperscaler marketplace term spikes at the same time, that signals a category-level shift.

Cloud commits crossed $500B last year. Multiple ISVs closed $2B+ on individual marketplaces. All 3 hyperscalers started positioning marketplace as a core revenue engine to partners and investors.

Marketplace moved from an alliances-team topic into sales, procurement and C-Suite.

The search data reflects what we all see in the field and in deal rooms.

Amazon Web Services (AWS) still is the benchmark

AWS has the strongest public proof of marketplace activity: the largest visible base of major ISV milestones, the deepest marketplace operating motion, and repeated evidence that enterprise software companies can scale very large numbers through AWS Marketplace.

Snowflake hit $7B total on AWS Marketplace. Salesforce crossed $5B. The list of ISVs past $1B includes ServiceNow, CrowdStrike and Adobe —and the list is growing.

Microsoft’s rebrand result is the biggest surprise

Microsoft merged Azure Marketplace with AppSource - its Dynamics 365, Microsoft 365, and Power Platform storefront — into one Microsoft Marketplace in Sep ‘25.

“Microsoft Marketplace” went from near-zero to the highest-trending marketplace term on the chart. Combined Microsoft marketplace search now rivals AWS.

AppSource brought in business-application buyers who never searched “Azure Marketplace” but now land in the same experience. AI users, Dynamics buyers, Microsoft’s broader commercial audience — all entering the marketplace.

The comparison with AWS and Google Cloud is not perfectly apples-to-apples — AppSource served a broader business-app audience beyond cloud. But the expansion of who searches for marketplace is exactly the point.

Google Cloud: smallest share, but fastest climb

Google Cloud Marketplace has the lowest broad search interest but has grown ~5X since 2021.

That tracks with Google Cloud’s revenue acceleration and $462B backlog. Palo Alto Networks crossed $2B on Google Cloud Marketplace — proof that strategic categories already produce large outcomes.

3 takeaways:

Marketplaces are mainstream. The spike across all 3 clouds means this is now a default enterprise buying behavior

Microsoft’s unification expands who buys through marketplace. ISVs on Microsoft now reach business-app and AI buyers alongside Azure infrastructure teams

GCP Marketplace growth creates an early-mover window. Fast-growing commit pool, and strong partner investment

What’s your strategy?

Join our AWS Marketplace Strategic Breakfast at AWS Summit NYC

Next week, we’re hosting the AWS Marketplace Strategic Breakfast at AWS Summit NYC. June 17. 7:30–9:30 AM ET, near Javits Center.

A focused, invite-only breakfast for senior alliance, marketplace, and cloud GTM leaders — with four senior AWS Marketplace leaders in the room and a lineup of ISV and ecosystem operators who are scaling on Marketplace right now.

Marketplace opportunity keeps growing

AWS customer cloud commitments reached $364B — spend that increasingly flows through Marketplace

99% of the top 1,000 AWS customers have at least one active Marketplace subscription

Buyers achieve 70% faster product discovery, 60% time savings in procurement, and 30% faster time-to-market (Forrester)

We’ll spend the morning with senior AWS Marketplace leaders and operators to break down the latest trends, buyer shifts, and execution patterns — and how companies should leverage them to scale in H2 2026.

Two AWS perspectives are especially worth highlighting:

George Maroulakos — Worldwide Leader of AWS Marketplace Center of Excellence, Buyer Experience.

Most of us focus on what we’re selling. George focuses on how customers are buying — and few people see buyer behavior, frictions, revenue growth, and change signals as closely as he does.

AI is compressing evaluation cycles and pushing buyers toward unified billing and outcome-based procurement. Marketplace is becoming the default front door for AI and enterprise software.

For ISVs and partners, this is where co-sell, pricing, private offers, and renewal strategy converge. George will explain how buyers navigate this — and how sellers can align with how buyers actually buy.

Michael Levy — Senior Manager, AWS Marketplace

Michael leads feature launch and adoption — the team driving business outcomes on AWS Marketplace for partners and customers.

He also leads GTM strategy for AI agents and tools in AWS Marketplace. This puts him at the intersection of the fastest-growing category in cloud and the fastest-growing procurement channel.

If you’re wondering how AI-native companies are approaching marketplace differently — or how traditional ISVs should position AI capabilities on Marketplace — Michael is tracking this closer than almost anyone.

Also joining as featured speakers

Arif Razvi — WW Leader, AWS Marketplace Business Development

Reagan Koryozo — WW Scale Adoption Specialist, AWS Marketplace

Whitney Bragg-Sabins — Senior Global Relationship Manager, AWS at ServiceNow

Trunal Bhanse — CEO, Clazar

David Mauer — VP of Channel & Alliances, LucidLink

Roman Kirsanov — Founder & CEO, Partner Insight

📅 June 17, 7:30–9:30 AM ET, at Oyamel restaurant New York (near Javits Center)

The room is curated and capacity is limited. Registration requires approval.

Thank you to our partners: Clazar, ServiceNow, and LucidLink for supporting this event.

LucidLink’s 39% Channel Engine: Rebuilt For Buyer Choice

39% of LucidLink’s revenue now runs through channel partners. That’s a number you would expect from an infrastructure or security vendor, not a media collaboration company. For LucidLink, that is exactly the point.

Their platform sits at the center of cloud storage, distributed production, and enterprise file workflows, where customers often need software, services, marketplace procurement, and tech partners to come together.

The shift to become partner-first took 13 months and a full rebuild of how LucidLink sells with partners.

“You never want a customer to tell you, ‘I want to buy through this partner, or I want to buy through this marketplace,’ and you have to say no.”

That line from David Mauer, VP of Global Partner Ecosystem, explains the logic behind LucidLink’s partner program relaunch.

If a customer asks to buy through a reseller, MSP, AWS Marketplace, or a systems integrator, the answer should be yes.

David Mauer joined LucidLink as VP of Channel and Alliances a year ago. He inherited a channel program that wasn’t pulling its weight.

In FY25, as the rebuild took hold, channel generated ~$5M in net new ARR, more than one-third of net new ARR.

FY26 plan is more ambitious: 45% channel mix of net new ARR

How do they do it?

Building Partner Architecture

In LucidLink’s original channel model, VARs could transact the product, but they hit a ceiling and couldn’t manage at scale. Marketplace was nascent and disconnected from the channel. Technology alliances didn’t bundle commercially. Each worked in isolation.

The rebuild was designed to clear every buying path the customer might need: reseller-led, AWS Marketplace, AWS co-sell, MSP-managed, technology alliance bundle, or enterprise direct.

LLMP: partners need operational control to drive revenue

LucidLink launched the LucidLink Management Platform (LLMP) to give partners the infrastructure to provision, manage, and bill LucidLink at scale across their customer base.

LLMP gives partners a structured view of partner-managed environments — visibility into customer state, contracts, and billing — so they can operate in confidence without escalating back to LucidLink.

“The channel isn’t an add-on to our strategy, it’s central to it. LLMP is about giving partners real operational leverage and differentiation with their customers.” — David Mauer

Cloud Marketplaces as the commercial backbone

LucidLink’s marketplace strategy sits inside the same architecture.

Amazon Web Services (AWS) is the anchor hyperscaler relationship today, with active marketplace and co-sell motion. Google Cloud and Oracle Cloud Infrastructure are part of the next phase of expansion.

The marketplace is not a separate transaction desk that sits next to channel.

Mauer’s team is building the partner program so marketplace, co-sell, channel, and technology alliances attach to the same customer motion.

That is how leading partner & cloud GTM programs are evolving

Read the full LucidLink case study here.

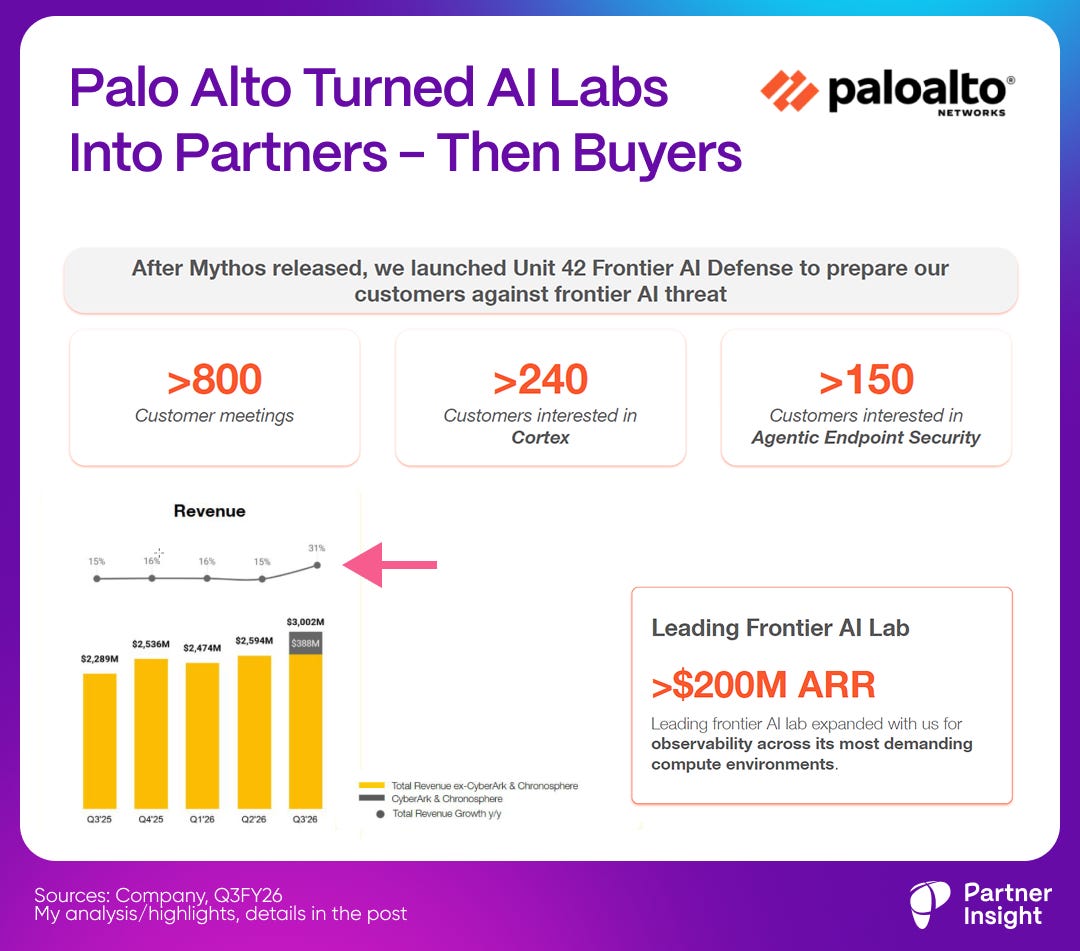

Palo Alto Turned AI Labs Into Partners - Then Buyers

Palo Alto Networks posted a record quarter last week: $3B revenue (+31% YoY), RPO $18.4B (+36%).

It’s striking how closely they now work with AI labs that many expected would disrupt them just months ago.

Four months ago, cybersecurity stocks crashed on AI fears

In February, Anthropic launched Claude Code Security. CrowdStrike, Datadog and Zscaler fell >10%.

The fear: frontier AI would automate vulnerability scanning and pen testing, making security platforms obsolete.

Then the same AI lab partnered with them

On April 7, Anthropic announced Mythos but refused to release it publicly.

Instead, Anthropic created Project Glasswing — giving a small group of security vendors early access to Mythos for defensive use.

Palo Alto was among the first partners. PANW stock surged 60% from that day.

Q3 shows how PANW turned this into a GTM engine

Arora:

“Leveraging our strategic partnerships with leading frontier labs, we utilize early access to their most advanced models to complete the equivalent of a year’s worth of pen testing in less than three weeks.”

That work created Unit 42 Frontier AI Defense — a new product that generated 1,200+ customer inquiries and 800 enterprise meetings in six weeks.

Those meetings aren’t staying in one product silo.

Arora confirmed they’re “driving conversations across the platform,” pulling demand into agentic endpoint security and broader platform deals.

AI labs aren’t just partners — they’re becoming major buyers

PANW crossed $200M+ in ARR with a single frontier AI lab for Chronosphere — their observability platform that monitors AI training and inference clusters at scale. Two of the top five frontier labs now run on it.

Arora:

“We surpassed $200 million in ARR with a leading frontier AI lab. We expect that to continue to grow next quarter.”

Prisma AIRS — PANW’s platform for securing AI applications and agents in production — tripled its customer base in one quarter (100 - 300+), with visibility toward $100M ARR. This product didn’t exist a year ago.

AI fears keep proving exaggerated

AI didn’t shrink cybersecurity’s addressable market. It expanded it — new threat surfaces, new traffic volumes, new identity complexity, and entirely new buyer categories that didn’t exist 18 months ago.

Yet again, the feared disruption became a growth catalyst. We will likely see the same pattern across enterprise software. AI will generate more ecosystem opportunities, not less.

For alliance leaders:

Study PANW’s playbook: partnership and co-innovation with a frontier lab - new product - 800 enterprise meetings - cross-platform pipeline. That partnership-to-GTM flywheel is replicable.

The “disruptor” can become both a partner and a buyer. Look for that dynamic in your own category.

AI capability shifts are expanding enterprise software TAM. Build your alliance strategy around where AI is growing your market.

How are you using AI to expand demand in your category?

P.S. Thanks for reading! If this issue sparked an idea, please forward it to your alliance lead or cloud counterpart — it’s how this community shares what works.