Why C-Suite Is 2X+ More Likely to Deploy Agentic AI With Partners

Hi, it’s Roman Kirsanov from the Partner Insight newsletter, where I deconstruct winning Cloud GTM strategies and the latest trends in cloud marketplaces.

In today’s edition:

AvePoint grew SaaS revenue 37% YoY in a market where many SaaS vendors are slowing. Their fastest-growing motion? Channel now drives 57% of ARR

Google Cloud commits jumped $155B → $240B in Q4 alone. Revenue from partner-built AI solutions grew ~300% YoY. Dai Vu, who runs GCP Marketplace, joins our event on March 24 to share what's next for partners.

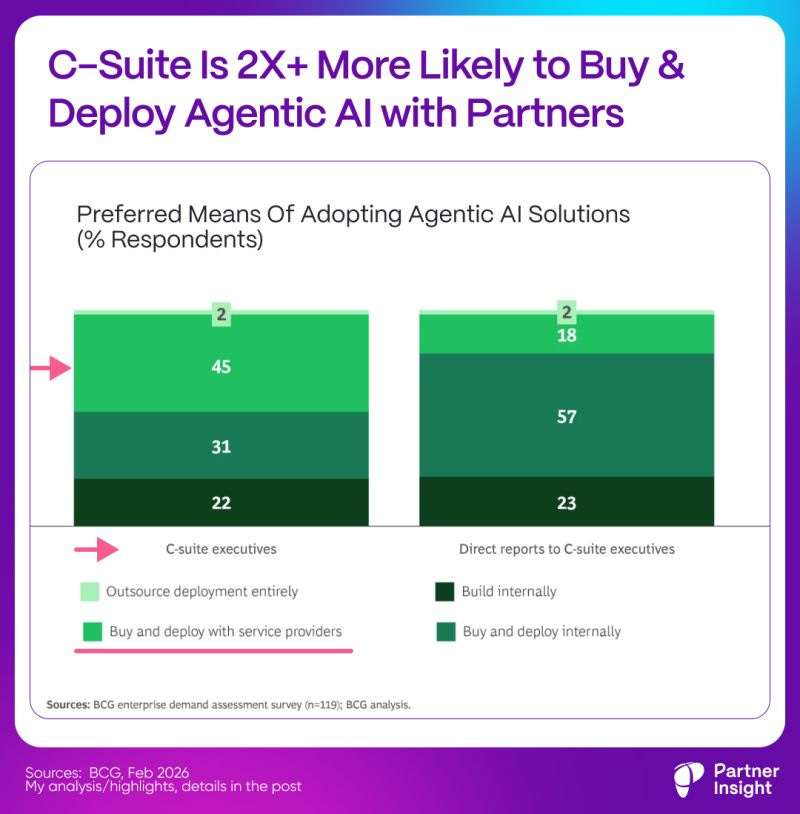

75% of enterprises want service providers to build their key Agentic AI use cases. Not internal teams. Partners. C-suite is also 2X+ more likely than mid-management to buy from partners.

Everyone says you need CEO buy-in for partnerships. Workiva’s CEO just showed what it actually looks like — and it’s more deliberate than most realize.

But first — if you sell through or alongside Google Cloud, don’t miss our biggest GCP online event of 2026:

Google Cloud Marketplace: Your Growth Engine for 2026 (March 24)

Dai Vu, Managing Director leading Google Cloud Marketplace, will share where Marketplace is heading next, what’s working for partners who are scaling, and how AI and co-sell motions are evolving in 2026. He’ll be joined by Jay McBain (Omdia), leaders from Palo Alto Networks, MongoDB, Optiv, Tackle and more. 10+ speakers. 2.5 hours.

Now, let’s dive in.

37% SaaS growth. 57% channel. AvePoint’s GTM playbook

AvePoint grew SaaS revenue 37% YoY to $88.9M in a market where many SaaS vendors are slowing.

Their fastest-growing motion? Channel now drives 57% of ARR

AvePoint builds data governance + protection software used by 28,604 customers across cloud platforms.

They hit $416.8M ARR (+27% YoY), with RPO at $508M (+36% YoY).

These are standout numbers, especially as market debates if AI will disrupt SaaS.

But the real story is how they sell.

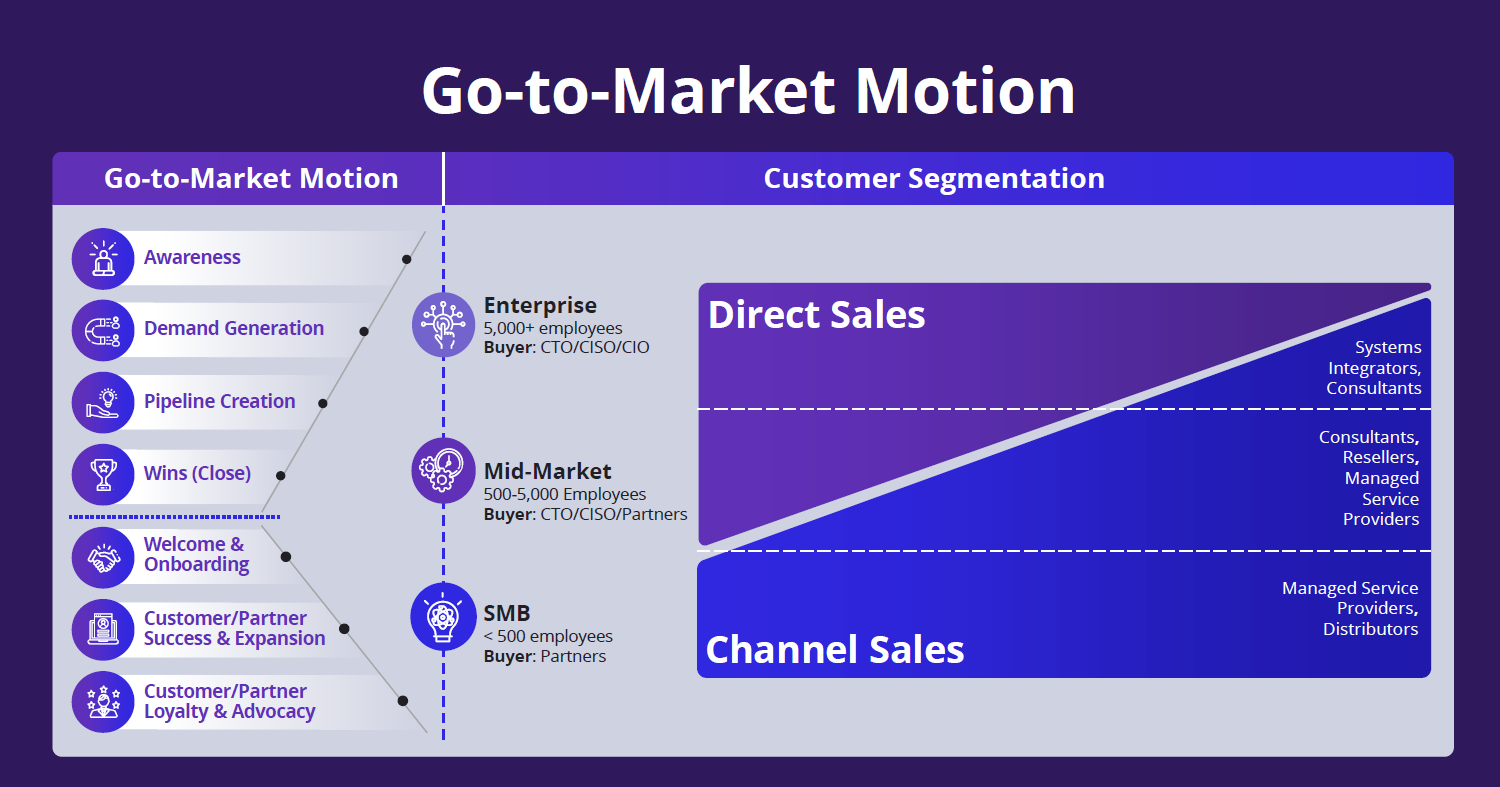

Their GTM breakdown

Enterprise (52% of ARR): primarily direct sales

Mid-market (28%): increasingly channel-led

SMB (20%): primarily through channel/MSPs

Channel growth in the last 3 years tells the story:

Channel ARR share: 47% (2022) → 57% (2025)

Channel partners: 3,403 → 5,859

MSP ARR: $19M → $62M (48% CAGR)

CEO Dr. Tianyi Jiang (TJ) last week:

“Our channel, focusing on MSPs, still our fastest-growing segment, unlocking SMB and mid-market. We have not seen slowdown in SMB, as some other vendors have seen.”

Channel isn’t just scale — it’s operating efficiency

Sales & marketing as % of revenue fell from 34.3% in FY24 to 31% in Q4 (and 32% for FY25).

AvePoint attributes this directly to scaling the channel strategy. They also hit Rule of 46 (ARR growth + operating margin), up from Rule of 31 two years ago.

Migration is the partner “tip of the spear”

AvePoint deliberately pushes services revenue to partners on migration projects, then retains the recurring software revenue on day-two governance, protection, and cost control.

Textbook land-and-expand through channel.

The hyperscaler GTM is expanding

AvePoint sells through Microsoft, Google Cloud, and AWS marketplaces, maintains strategic partnerships with all three clouds, and is moving beyond Microsoft 365 into multi-cloud workload governance across compute infrastructure.

They also signed a $340M five-year IT services consumption commitment (2026-2030) — a signal of how deeply embedded they are in hyperscaler economics.

AI doesn’t reduce their customer needs — it amplifies them

LLMs don’t eliminate security, backup, compliance, and policy control. They raise the stakes.

AvePoint is leaning into that with agent control / AI governance and pricing that mirrors hyperscaler economics: a blend of seat + consumption.

3 takeaways for alliance leaders:

Map partner strategy by customer segment. Clarity on “who sells to whom” prevents conflict and lets each motion scale.

Channel drives margin improvement, not just reach. Track S&M % of revenue as your channel matures — it’s the cleanest proof point for your CFO.

Treat hyperscalers as ecosystem opportunities for GTM: align marketplace procurement + co-sell + partner delivery into one motion

What’s your experience — does driving partners revenue accelerate customer adoption and stickiness?

Dai Vu, Who Leads Google Cloud Marketplace, Keynotes Our Biggest GCP Event of 2026

Google Cloud customer commits jumped $155B → $240B in Q4 alone. Revenue from partner-built AI solutions grew ~300% YoY.

Dai Vu, Managing Director leading their Marketplace, will share what’s next in our biggest GCP event of 2026.

If you sell software through or alongside Google Cloud, Dai Vu is shaping how that entire market works.

His keynote in our GCP online event on March 24 is the closest you’ll get to Google’s Marketplace strategy before Next season.

Dai Vu leads the global teams behind Google Cloud Marketplace — business development and P&L, partner and platform strategy, co-sell and field GTM models, partner engineering and enablement.

Under his leadership, GCP Marketplace has been growing triple-digits YoY for multiple years, driving billions in transaction value annually.

This will be Dai Vu second keynote at our event. A lot has changed since last year.

Google Cloud momentum is hard to ignore

Revenue grew incredible 48% YoY last quarter

Annual run rate crossed $70B

Cloud commitments (RPO) jumped to $240B — committed customer spend that can be used on its marketplace to buy ISV partner products

On the partner side, the signals are even more striking

Revenue from AI solutions built by partners grew nearly 300% YoY

Commitments from Google’s top 15 software partners increased 16X+ YoY

Customer adoption is impressive

New customer velocity doubled in Q4 vs Q1

$1B+ customer deals in 2025 exceeded the previous 3 years combined

Existing customers are outpacing initial commitments by 30%+

~75% of Google Cloud customers have used their vertically optimized AI – from chips, to models, to AI platforms, and enterprise AI agents

The ecosystem around Google Cloud is expanding fast — and the co-sell + marketplace math is changing for every ISV and partner on the platform.

Dai will share where Marketplace is heading next, what’s working for partners who are scaling, and how AI and co-sell motions are evolving in 2026.

The all-star lineup joining him

Jay McBain, Chief Analyst at Omdia — the most accurate voice on cloud marketplaces, who forecasted $85B marketplace opportunity years before the industry caught up. Jay sees marketplaces reaching $163B by 2030 with 59% of deals flowing through channel partners

Leaders from Palo Alto Networks ($2B+ in GCP Marketplace sales), MongoDB (3X GCP Partner of the Year), Google Cloud, Optiv, Tackle and more

Two panels on co-sell strategy and channel ecosystem growth, plus operations deep dive focused on marketplace automations and scaling revenue efficiently

10+ speakers. 2.5 hours. Entirely free.

This event is just 4 weeks before Google Cloud Next. This is your chance to learn directly from the people leading the distribution on GCP marketplace platform — and know exactly where to focus in 2026 before the big Next announcements start.

March 24, 9:00–11:30 AM PT

See you on March 24th.

Thanks to our partner Tackle for supporting this event

Tackle (now part of AppDirect) is the Cloud GTM platform built to help software companies win in the cloud. As the category creator and leader in Cloud GTM, Tackle enables ISVs to list, transact, and scale through the hyperscalers.

Tackle streamlines every stage of the cloud marketplace journey with deep co-sell automations, private offer management, and real-time marketplace analytics.

Together with AppDirect's global subscription commerce platform, Tackle is building the first truly unified solution for software companies to reach buyers across every route to market: cloud marketplaces, direct sales, and the channel.

C-Suite Is 2X+ More Likely to Buy & Deploy Agentic AI with Partners

75% of enterprises want service providers to build their key Agentic AI use cases. Not internal teams. Partners.

And C-suite is leading the charge, 2X+ more likely than mid-management to buy from partners.

Everyone’s asking the same question: will Agentic AI gut tech services revenue? BCG just surveyed 190+ execs on both sides - enterprise buyers and partners - and the data tells a very different story

This isn’t a shrinking market

BCG projects Agentic AI will unlock up to $200B in net new demand for tech services over the next 5 years (6–8% CAGR through 2030).

AI efficiency-led losses in traditional contracting are real but localized. The new value pools — building, deploying, running, and governing AI agents — are much larger for partners to grasp.

Winning service partners are orchestrating ecosystems

“More than 90% of providers report delivering Agentic engagements leveraging ecosystem partners. The competitive advantage lies in orchestrating these partnerships to accelerate deployment, standardize patterns, and scale proven use cases.”

Winning service partners aren’t just reselling or implementing. They are orchestrating multi-partner ecosystems — hyperscalers, SaaS platforms, and emerging agentic-native players — into repeatable, scalable deployments.

What’s the state of Agentic AI deployment by enterprises right now?

40%+ of large enterprises are already scaling Agentic AI beyond pilots. Banking, financial services, and insurance are leading. “2026 is shaping up to be a pivotal year” from experimentation to enterprise-wide deployment.

Agentic AI investment has grown 60%+ annually since 2023, with over 55% flowing into agent platforms and orchestration layers — the infrastructure that hyperscalers and their partners are building together.

Agentic components now show up in 40%+ of enterprise sourcing cycles across IT applications, BPO, and CX services.

Pricing model mismatch favors marketplaces

One gap remains: >70% of enterprise buyers want output- or outcome-linked pricing for agentic services. Yet ~60% of providers still contract on time-and-materials or fixed-price.

It seems cloud marketplaces — with consumption-based and usage-linked commercial models — are naturally positioned to close this gap.

Three lessons for alliance leaders:

Treat Agentic AI as a new growth category to capture WITH your ecosystem — new offers, partners, new routes to market — not just a margin or efficiency play

The competitive edge isn’t building agents alone. It’s orchestrating hyperscaler, ISV, and SI partnerships into packaged use cases that enterprises can deploy fast

The buyers who matter most — C-suite — are choosing partners over internal builds and are betting on ecosystems. Your sales and marketplace motions should match those executive-level buying patterns

What’s your take — is Agentic AI a threat to existing revenue, or an expansion of your TAM?

Source: Research.

CEO Buy-In for Partnerships: “I only highlight wins that involve our partners”

Everyone says you need CEO buy-in for partnerships.

Workiva’s CEO just showed what it actually looks like — and it’s more deliberate than most realize.

Last week I published an analysis of Workiva’s strategy. They’re growing 21% YoY with partner-driven GTM.

Every single one of the 14 enterprise deals their CEO mentioned in Q4 earnings call involved a partner — co-sold, sourced, or implemented.

The post got traction. But what happened next was even more interesting.

Workiva’s CEO Julie Iskow commented directly:

“It wasn’t just 14 out of 14 in our recent earnings. Every earnings call I only highlight wins that involve our partners. It’s intentional. Our high-performing partner ecosystem is key (and vital) to our success”

Let that sink in.

The CEO of a public company approaching $1B in revenue deliberately chooses to ONLY spotlight partner-involved wins on the most visible public stage of the quarter.

This is not a partnership slide in a board deck.

This is the CEO using the earnings call — the moment when Wall Street, customers, and employees are all listening — to send an unmistakable signal about what matters.

And signals like that cascade

When a CEO consistently highlights partners publicly, it shapes:

how CROs build sales motions

how sellers prioritize co-sell

how marketing tells the story

how product thinks about ecosystem leverage

how the company allocates resources

Example:

Workiva new CRO, Michael Pinto (ex-AWS and Databricks), was brought in with an explicit mandate to strengthen their partner ecosystem. That hire doesn’t happen without top-down commitment.

Julie also added a second point most partnership narratives miss:

“Our partners don’t just “help us close deals, find opportunities and own implementations”. They also help our customers get more value from our platform ... and ultimately other solutions (a win-win-win: for our partners, our customers and Workiva).”

This framing matters.

At Workiva, partners aren’t just a distribution channel — they’re customer success drivers. And In the AI era, that distinction is everything: partner-led implementations and services accelerate time-to-value, increase adoption, and unlock expansion — making outcomes stickier and relationships harder to unwind.

The takeaway: C-suite commitment to partners isn’t a nice-to-have. It’s one of the highest-leverage inputs into ecosystem-led growth.

3 things alliance leaders can take from this:

CEO buy-in isn’t a one-time decision. It’s a repeated, visible signal — every quarter, every earnings call, every internal moment.

Ecosystem depth is the moat in the AI era. Partners who implement, enable, and expand your product drive stickiness that features alone rarely do.

Watch what executives highlight publicly, not just internally. Earnings calls, keynotes, and analyst days reveal real priorities.

Do partners show up in your company’s most visible internal and external narratives?

P.S. If you found these insights valuable, please forward this newsletter to your alliance lead or cloud/GTM counterpart - it’s how this community shares what works.